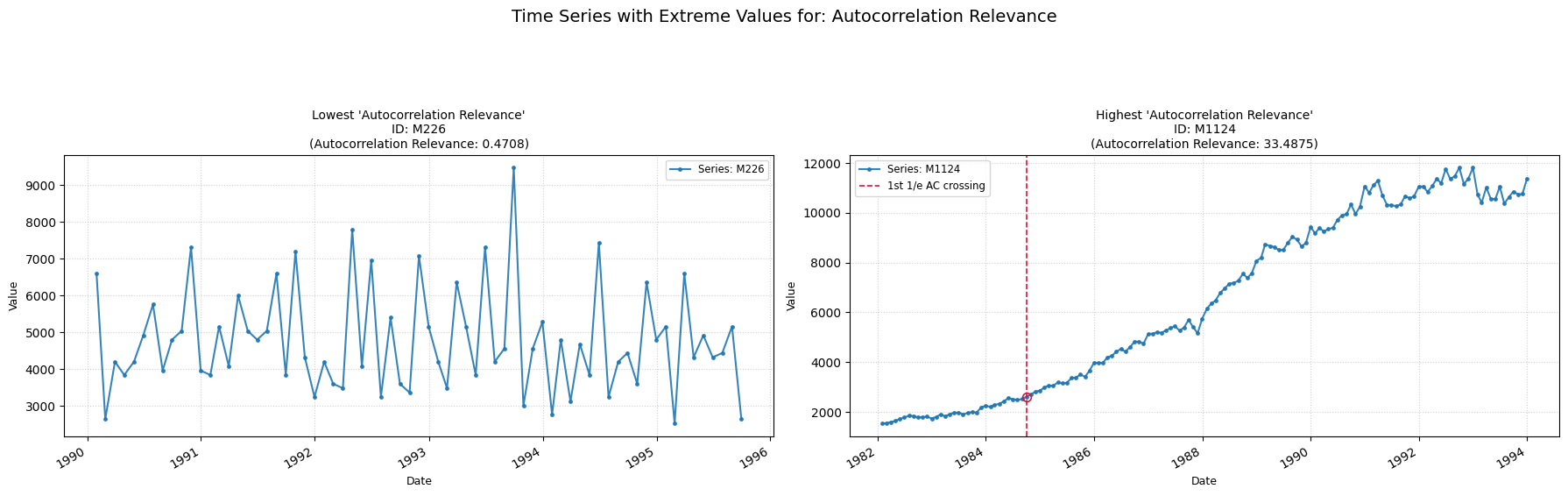

Autocorrelation Relevance

ac_relevance

Measures the first time lag at which the autocorrelation function drops below 1/e.

Low value: Means the series has a more unpredicatble behaviour.

High value: Means the series has a more predictable behaviour.

No Parameters

Calculation

-

Autocovariance Function (ACVF): The autocovariance function of the time series Yt is computed for various lags k.

-

First 1/e-Crossing: The feature value is computed and returned as the smallest positive for which ACVF(k) crosses the defined 1/e threshold.

Practical Usefulness Examples

Speech Processing: In analyzing a speech signal, the first zero-crossing of the autocovariance can be related to the fundamental frequency (pitch) of voiced segments, helping in speech recognition or speaker identification.

Climate Science: For temperature data, this feature might indicate the dominant short-term cyclical component (related to diurnal cycles if data is high frequency, for example).