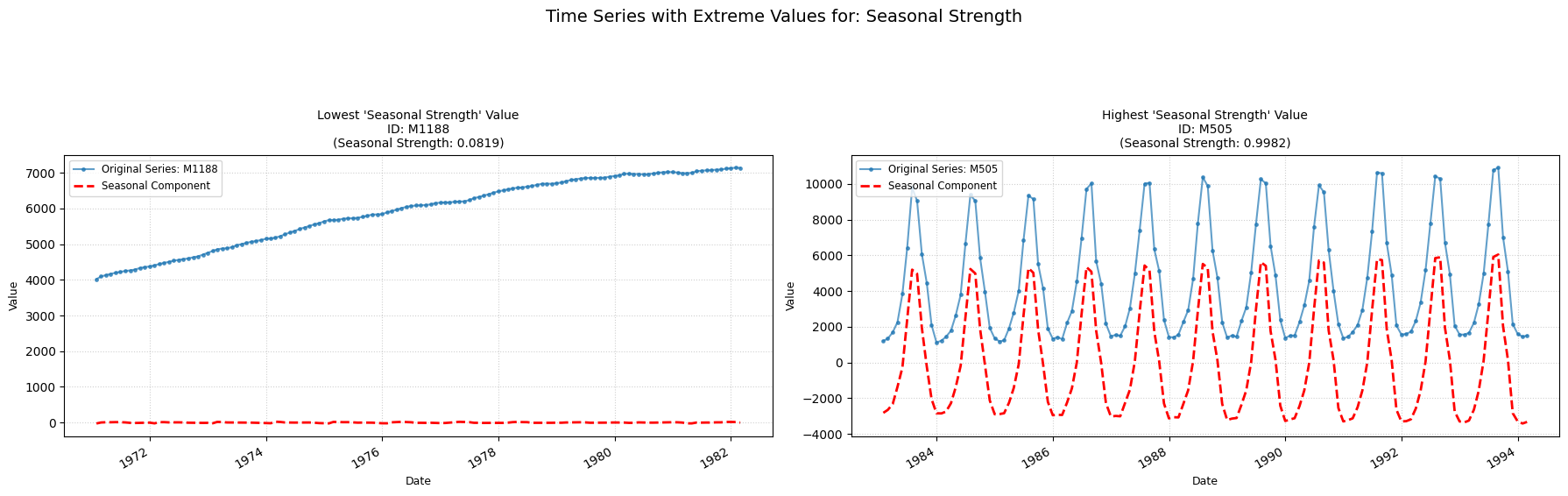

Seasonal Strength

seasonal_strength

Computes the strength of seasonality within the time-series.

Low value: A value close to zero means there are few/none indicators of seasonality in the time series.

High value: A value close to one means there are strong signs of seasonality in the time-series.

Parameters Table

| Parameter | Type | Default | Description |

|---|---|---|---|

| period | int | 1 | Frequency of the time series (e.g. 12 for monthly) |

| seasonal | int | 7 | Length of the seasonal smoother (must be odd). |

| robust | bool | False | Flag for robust fitting. |

Calculation

-

STL Decomposition: The time series Yt is decomposed into trend (Tt), seasonal (St), and remainder (Rt) components, using an STL decomposition.

-

Detrended Series: The detrended series is calculated as Yt′=Yt−Tt=St+Rt.

-

Variances Calculation:

- The variance of the remainder component is calculated: Var(Rt).

- The variance of the detrended series is calculated: Var(Yt′).

-

Seasonal Strength Calculation: The value for seasonal strength is computed as max (0, 1 − Var(Yt′) * Var(Rt)). This value is capped between 0 and 1 and returned.

Practical Usefulness Examples

Retail Demand Planning: A high seasonal strength for ice cream sales (peaking in summer) allows a company to confidently plan production and marketing efforts around these predictable peaks and troughs.

Tourism Industry: Hotels can use the seasonal strength of booking data to optimize pricing, staffing and promotions, anticipating high and low seasons.